David Leonardt in the New York Times has a great chart breaking down the job growth in 2010 and what that means for the shape and duration of the recovery. The general picture is not new, but the way it is described is quite useful and insightful.

o get ugly.

o get ugly.

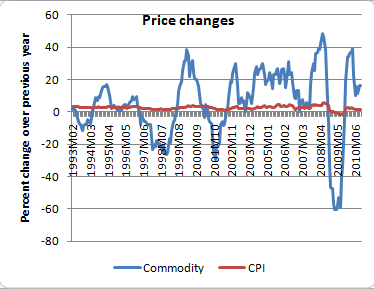

There are two points to note on the chart. First, it clearly shows the deflationary effects of the credit crisis - the rate of deflation was worse than that of the early Great Depression (that deflationary period set off a vicious cycle that led to later deflation). The second point is how, in the longer run, the more recent deflation problem has been relatively small - until recently. The big question is whether this recent downturn (last three months) will continue. The high level of unemployment and low consumer confidence are not encouraging.

From the perspective of teaching, I really like the chart above because of the comparison it sets up. My students are seniors, so they have had U.S. History and know about the Depression. A chart that sets up a comparison is good because it gets the students thinking about what might be different this time. While lots of things are different, the biggest difference is policy. The halt of deflation in the months after the credit crisis was the result of very active monetary and fiscal policy. The point of the chart it that it demonstrated that these policies worked - in the sense that they put off economic collapse.

A good question to ask students is how to use the information in the chart to forecast where the economy is going and what, if any, policy should be enacted. In other words, should the Fed be more aggressive in an easy money policy and should there be more fiscal stimulus, since both policies would be inflationary (or at least anti-deflationary). Getting students in the practice of forecasting and thinking about policy is getting them to do what economists do.